From the National Federation of Independent Business

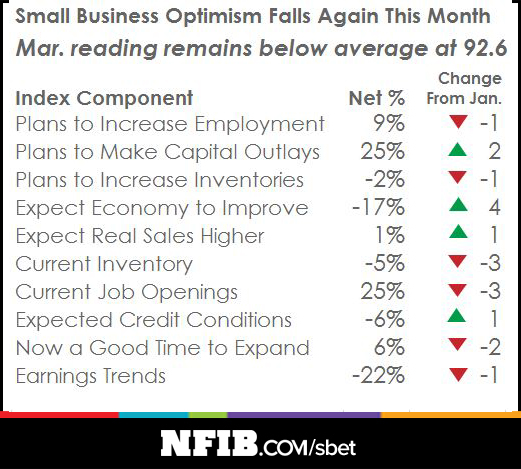

The Index of Small Business Optimism fell 0.3 points from February, falling to 92.6. Statistically, no change. Four of the 10 Index components posted a gain, six posted small declines, the biggest gain was in Expected Business Conditions, a 4 point improvement to a still very negative number. The market was expecting the index between 93.5 to 93.9 with consensus at 93.6 – versus the actual at 92.6.

NFIB chief economist Bill Dunkelberg states:

Small Business owners remain extremely pessimistic about the economy, and rightfully so. Cost-increasing regulations seem to multiply overnight and there is no clear end in sight.

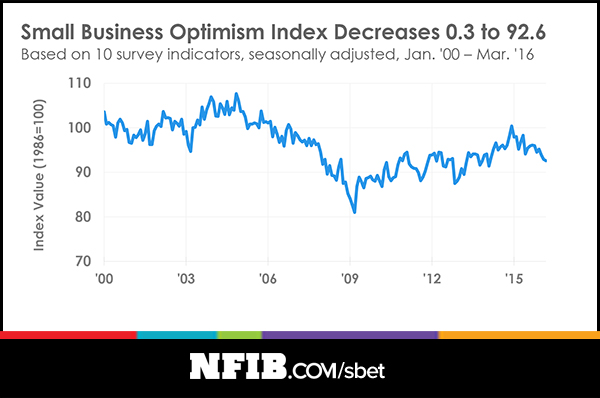

The overall Index dropped 0.3 points in March and now stands at 92.6. The reading was not a huge statistical change, but still slid below the lowest reading in two years and is well below the 42-year average of 98. Four of the 10 Indices posted a gain and six posted declines. The largest gain was in Expected Business Conditions. Despite a 4 point improvement, only a net negative 17 percent of business owners expected business conditions to improve in the next six months. The political climate continued to be the second most frequently cited reason, after a weak economy, for why a seasonally unadjusted 51 percent of owners think that the current period is a bad time to expand.

Arbitrarily raising the cost of labor reduces employment opportunities and raises prices. This just gives small firms an incentive to find ways to use less labor.

For a broader perspective, the Index has turned decidedly “south” over the last 15 months. The reading has fallen from 100 in December of 2014 to the current 92.6. A recession warning signal is flashing and that next month’s survey could determine whether or not the alarm should be rung.

The mess we are in is the cumulative result of decades of attempts to redistribute income with volumes of taxes and regulations.

Report Commentary:

Apparently, New York Federal Reserve President (and FOMC Vice Chair) William Dudley’s walk back of prospects for a second rate hike in Hangzhou last month was not satisfactory, so Chair Yellen added her support to keeping the status quo. Financial markets applauded, but the real sector did not, with consumer and small business sentiment falling.

Financial markets of course thrive on the variability such policy pronouncements and policies produce. Bonds have been made very unattractive by Federal Reserve policy, so equities are the only game in town that might promise a yield. Low interest rates are great if they occur in an economy that presents investment opportunities. This is not the case for our current economy. There is no cheerleader for the economy who convincingly promises improvement. There is little hope that government will constructively address the problems that concern consumers and small businesses. The most likely prospects to assume the presidency don’t appear to be connected to reality. There is no prospect that the avalanche of resource-wasting regulations will abate much less be reversed. The “experts” at the Federal Reserve only raise uncertainty with their pronouncements and seem detached from the real economy, focused instead on financial markets. Two of our largest states have passed a $15 minimum wage, preventing millions of lower skilled and young workers from ever getting their first job. None of this makes sense to Main Street businesses or many consumers who think government economic policies are “bad” by a 2 to 1 margin. The “mess” we are now in is the cumulative result of decades of misdirected, special interest policies, attempts to redistribute income and manipulate private sector firms with volumes of regulations and taxes.

The Fed continues to confuse and confound. It is unsettling that the Fed (a) is trying to create inflation when historically managing inflation was the central bank’s job (b) will do anything, including negative interest rates, to pursue this 2% objective without questioning the sense of it and (c) continues to think that its low interest rate policy will create jobs when the uncertainty the Fed creates holds spending back. Low rates are not sufficient to stimulate hiring and spending if investing in workers or new capital shows little promise of paying off. The Fed has not been able to attain either its goal of 2% inflation or “maximum employment” (whatever this is) with its policies, yet it keeps on going (remember the definition of insanity?).

The small business sector, which historically produced half of our private GDP and served as the “R&D” sector of our economy (this is where new ideas are tested by markets, the proper evaluator, not government), is underperforming, doing little more than operating in maintenance mode. Slow economic growth is now just a result of population growth, more haircuts, retail customers, health care patients, etc. But there is no exuberance, no optimism and not much hope, the numbers make it clear. Owners have been able to borrow at low rates for nearly a decade but most have no interest in borrowing because government policies have stifled economic growth and the potential for investment in real capital to yield a decent return.

No Comments