Source: CNBC

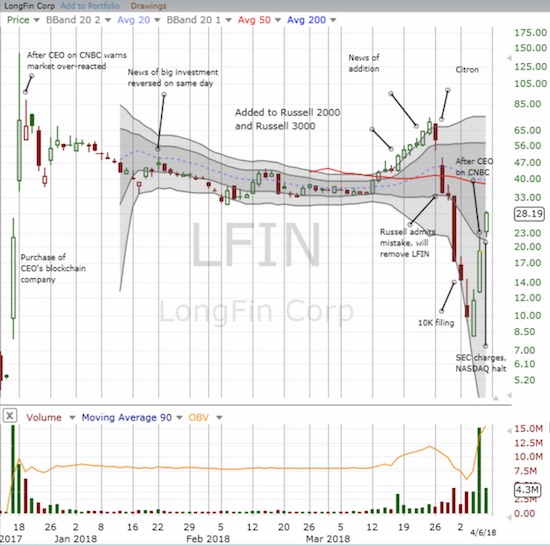

On Friday, April 6th, Longfin Corp. (LFIN) rallied 47% right into a trading halt.

Ever since LongFin Corp. soared astronomically four days into its stint as a publicly traded company, I have been fascinated by the story. At the time I covered the rally, I wrote: “The trading in recent IPO LongFin Corp. may go down as iconic in this era of frenetic trading in almost anything related to cryptocurrencies and blockchains.”

Since then, LFIN has become more iconic than I could imagine: the stock and the company are hyper-emblematic of the tremendous distortions that can occur in the middle of manias.

Source: FreeStockCharts.com

Like an air puppet, Longfin Corp. has soared, twisted, and flopped wildly in just 4 months of headline-laced trading action.

Just over a month into being a publicly traded company and then 70% below its intraday all-time high, LFIN proudly announced a major investment in the company that it promptly retracted the very same day. This behavior was strange enough – after all, the CEO admitted earlier that the company was overvalued at its lofty levels. The willingness of investors to sit on the company’s post-news premium struck me as even more strange. Some semblance of “normalcy” seemed to get going as LFIN drifted lower for 2 weeks. Yet, soon after options began trading on LFIN, the stock stabilized for another month until the news got bizarre all over again. THIS spate of news may be spelling the final throes of this company.

Russell unravelling

LFIN announced on March 22nd that its stock was added to the Russell 2000 and Russell 3000 small-cap indices. The addition apparently happened on March 16. All of us who watched in amazement as LFIN marched steadily higher on no news suddenly understood what was driving the stock. Index funds were adding LFIN to their coffers to prepare for the index change. The news seemed to herald LFIN’s undoing. LFIN caught the attention of short-sellers, like the infamous Citron, and LFIN’s story quickly unravelled from there.

The day after Citron’s hit, Russell admitted its mistake in adding LFIN to its small-cap indices. That news caused an implosion of LFIN’s stock. In one day, ALL the gains of the March breakout were erased. Next up came a 10K filing on April 2 that disclosed an SEC investigation. While that alone was bad enough, the immediate reporting in the financial press skipped over other troubling elements of this report: 1) LFIN blamed short-sellers for the trading woes in its stock, 2) LFIN claimed a Seeking Alpha article convinced FTSE to remove LFIN from its small-cap indices, 3) LFIN established that its cryptocurrency token has no intrinsic trading value, 4) the company described the volatile trading in its stock through March 30th as a “trading bubble,” 5) LFIN disclosed material questions over whether it can continue as a going concern, and 6) LFIN admitted lax financial controls. Points #1 and #2 above are mere deflections from the serious issues contained in points #5 and #6. Points #3 and #4 further undermine the rationality of the LFIN’s current stock price.

In a section titled “Techniques employed by manipulative short sellers in cyptocurrency[sic] stocks may drive down the market price of our common stock,” LFIN explained how short-selling works and how it works against a small company like LFIN. The company blamed the attack on its company as the result of an unregulated ability of short-sellers to publish their claims. LFIN warned: “You should be aware that in light of the relative freedom to operate that such persons enjoy, in case of a short-seller attack, our stock may suffer from a temporary, or possibly long term, decline in market price should the rumors created not be dismissed by market participants.” I would have thought the company would rely on itself, and not market participants, to defend the business against false claims.

LFIN’s claim that the FTSE was in error for removing the company from the Russell indices was particularly bizarre: “…a report published on the Seeking Alpha website on March 23, 2018 alleged that the addition of our Class A Stock to the Russell 2000 index was in error, which led to our Class A Common Stock being removed from the Russell 2000 index.” In LFIN’s view, the article was responsible for the index removal and not the recognition of a legitimate mistake. LFIN CEO Venkat Meenavalli promptly told CNBC that the company would reapply for inclusion based on the increase of its free float “…above the minimum 5 percent as of March 11 due to the expiration of a lockup period on a consultant’s stock holdings.” Of course inclusion in an index may be the least of the company’s concerns with an SEC investigation underway.

No Comments