Latest Posts

-

Finance 0

Yen & VIX Continue Lower

With US indices continuing to march ever higher, no surprise to see our Yen complex of pairs move strongly upwards, and bearish sentiment in the Yen index gather momentum. Of the pairs we track the commodity yen crosses have been particularly bullish, and reflecting further current risk off market sentiment, with cad/jpy also benefiting from a rise in the price of oil. From a trading perspective it has been very much a case of going with flow as Yen selling shows little sign of coming to halt. Moving to the Yen index, yesterday’s price action on the daily chart saw the index break through key support at 7550,and with the Nikkei225 also push... -

Finance 0

U.S. Dollar Checks, Bounces From Support On NFP Disappointment

Coming into this morning’s Non-Farm Payrolls report out of the United States – a glimmer of hope had developed for U.S. Dollar bulls as the Greenback continued to respect the support that was established earlier in the week. Prices had trickled up to the first resistance level we had looked at in yesterday’s article, but as the actual data came-in quite a bit below expectations, sellers came back to take DXY prices from resistance almost directly to that same area of support. This morning’s Non-Farm Payrolls number came in at +146k versus the expectation of +190k. This was led by large losses in the retail sector, and this constitut... -

Finance 0

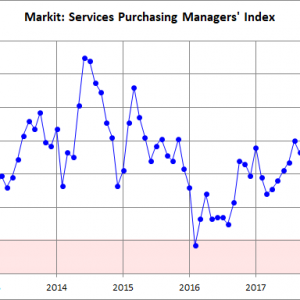

Markit Services PMI: Business Activity Growth Softens In December

The December US Services Purchasing Managers’ Index conducted by Markit came in at 53.7 percent, down 0.8 from the final November estimate of 54.5. The Investing.com consensus was for 55.9 percent. Markit’s Services PMI is a diffusion index: A reading above 50 indicates expansion in the sector; below 50 indicates contraction. Here is the opening from the latest press release: December data signalled a solid, but softer expansion in business activity across the US service sector. Moreover, the latest upturn eased to a seven-month low. In line with the trend in output, the rate of growth in new business volumes softened slightly. ... -

Finance 0

Weak Services Report And Dovish Comments Weigh On The Dollar

After the disappointing Non-Farm Payrolls only temporarily hurt the US dollar, the greenback received two more blows. The ISM Non-Manufacturing PMI, which is usually a hint towards the NFP, was released 90 minutes afterward, and missed expectations: a fall from 57.4 to 55.9, below 57.6 that was expected. The employment component actually advanced and it proved to be unreliable as an indicator. The other hit came from Patrick Harker, the president of the Philadelphia Fed. He said that two hikes are appropriate in 2018 and that is lower than 3 hikes that are suggested by the dot plot that the Fed released in its December decision. EUR/USD wa... -

Finance 0

US Services Sector Slumps As New Orders Crash Most Since Lehman

Confirming the mixed picture from Markit (Manufacturing PMI up, Services PMI down), ISM Services printed a disappointing 55.9 (57.6 exp), dropping to a 4-month low (as ISM manufacturing rises). Perhaps most notably, New Orders have utterly collapsed in the last 2 months post-Hurricanes… Additionally, Business Activity fell, as did backlogs…but there is quite a difference between manufacturing and services surveys… Respondents remain mixed: “Many suppliers are proposing price increases, but few are being implemented. Increases in volume and efficiencies seem to be outperforming commodity pricing.” (Accommodati... -

Finance 0

Ever Been Part Of A Melt-Up?

This morning I noted that I did not appreciate seeing Jeremy Grantham’s note dismissed even in the slightest way and without rancor by a Biiwii author. His intro was “Here we go with the “melt-up” meme again.”, which I felt was not appropriate for our purposes, coming as it did from a writer who was cautionary all through 2017. Look, I was pretty sure I was going to be wrong about a Q4 market top long before Q4 ended. I was led to believe that through subsequent information and analysis, most notably delivered by the 3 Amigos, who will ride bullish until their respective journeys end. At the time of the Q4 cycle forecast how... -

Finance 0

Student Debt Slavery II: Time To Level The Playing Field

This is the second in a two-part article on the debt burden America’s students face. Read Part 1 here. The lending business is heavily stacked against student borrowers. Bigger players can borrow for almost nothing, and if their investments don’t work out, they can put their corporate shells through bankruptcy and walk away. Not so with students. Their loan rates are high and if they cannot pay, their debts are not normally dischargeable in bankruptcy. Rather, the debts compound and can dog them for life, compromising not only their own futures but the economy itself. “Students should not be asked to pay more on their debt than they ca... -

Finance 0

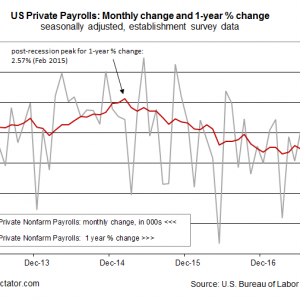

US Payrolls Growth Unexpectedly Cooled In December

Corporate payrolls in the US increased by less than expected in December, rising 146,000 in 2017’s final month — well below November’s strong 239,000 rise, according to this morning’s monthly employment report from the Labor Department. Economists were looking for a stronger rise: 185,000 via Econoday.com’s consensus forecast. The softer gain kept the year-over-year trend unchanged at a modest pace, which suggests that the labor market in 2018 may face stronger headwinds than previously assumed. Companies lifted payrolls by 1.64% for the year through last month, matching the annual rate in November. That’s still a healthy pace, ... -

Finance 0

Gold Bulls – Gotta Love This Pattern Says Joe Friday

In 2011 the Power of the Pattern suggested that Gold could be flat to down for years to come. See post here. Since that post in 2011, Gold finds itself down around 30% and Silver is down over 65%. 2011 saw extremes in prices. After nearly 7-years of lower prices, could the trend in metals be about to change? Below looks at chart of Gold and the US Dollar over the past 27-years- This chart reflects the “potential” that the US Dollar could be creating a bearish head & shoulders topping pattern, while Gold could be creating bullish inverse head & shoulders bottoming pattern. Joe Friday Just The Facts- The odds might be low that... -

Finance 0

November 2017 Trade Balance Marginally Worsened

Trade data headlines show the trade balance marginally worsened from last month. Analyst Opinion of Trade Data The data in this series wobbles and the 3-month rolling averages are the best way to look at this series. The 3-month averages are increasing for exports and increasing for imports… The data is much worse if one considers inflation is grabbing hold in exports and imports – and the headline numbers are not inflation adjusted. Import goods growth has positive implications historically to the economy – and the seasonally adjusted goods and services imports were reported marginally up month-over-month. Econintersect�...

Top Posts

-

The Importance for Individuals to Use Sustainable Chemicals

The Importance for Individuals to Use Sustainable Chemicals

-

Small Businesses: Finding the Right Candidate for the Job

Small Businesses: Finding the Right Candidate for the Job

-

How to Write the Perfect Thank You Letter After Your Job Interview

How to Write the Perfect Thank You Letter After Your Job Interview

-

3 Best Large-Cap Blend Mutual Funds For Enticing Returns

3 Best Large-Cap Blend Mutual Funds For Enticing Returns

-

China suspected in massive breach of federal personnel data

China suspected in massive breach of federal personnel data

New Posts

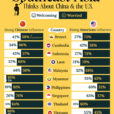

Charted: What Southeast Asia Thinks About China & The U.S. What Southeast Asia Thinks About China & the U.S. Feelings Towards China Feelings Towards America

FX Speculators Reduce Bearish Bets For Yen, Canadian & Australian Dollars Weekly Speculator Changes led by Canadian & Australian Dollars Speculators reduce bearish bets for Yen, Canadian & Australian Dollars Currencies Net Speculators Leaderboard Strength Scores led by Mexican Peso & Bitcoin Bitcoin & Australian Dollar top the 6-Week Strength Trends

Decoding Market Structure With Volume Profile

Flush Money Market Funds Typically Mean Rally

Cannabis Stocks Dropped 19%, On Average, In Last 3 Days Of This Week